India's Third Giant Leap

This Could be One of the Biggest Opportunities for Investors

Power Stocks: Long Term Wealth Creators

Image source: Daniel Balakov/www.istockphoto.com

Image source: Daniel Balakov/www.istockphoto.comFor almost two decades since the year 2000, China's power demand increased at a compounded rate of 9.4%. At the same time, GDP compounded at 8.7%.

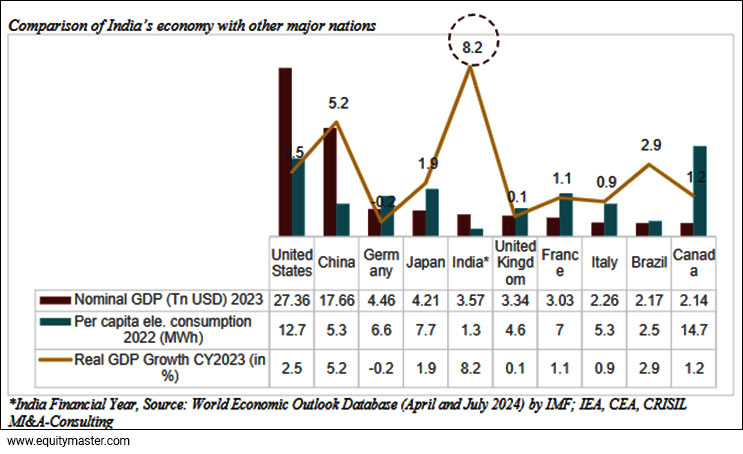

Historically, power demand in China has grown by 1.1x GDP.

India's power demand has been 0.9 times the real GDP growth. In the last three years, though, the multiplier for India averaged 1.2x.

There is good reason to believe that India power multiplier ratio will be a critical indicator of India's economic trajectory in the coming decade.

India's electricity consumption per person rose to 1,331 kWh in FY23. This was led by increase in manufacturing activity, rising domestic consumption, rural and household electrification, and extended hours electricity supply.

Globally, electrification of automotive energy has been a key driver of power demand. Further, to reduce the share of fossil fuels and meet the net zero emission status in 2050, electric mobility needs to rise to 30% by 2030.

As per Ola Electric, in India, electrification is most evident in the 2-wheeler space, which would see EVs account for 50% of total sales by FY28.

But EVs are not the only power guzzlers. Rising per capita income in India is driving higher household ownership of electrical appliances, like air conditioners.

Then comes manufacturing automation. Factory shopfloors in India are undergoing a significant transformation to cope with the requirements of globalisation, shorter product life cycles, changes in market & demand, and rapid technology advancements.

We are witnessing manufacturing companies transitioning from rugged machinery workshops to flexible and reconfigurable systems. This is to reduce the lead time between different products.

The goal is also to connect humans and machines (smart systems) to achieve flawless flexibility and agility at the lowest possible cost.

This involves the adoption of both hardware and software technologies including IoT (Internet of Things) devices, RFID systems, and smart sensors on machinery that allow real-time data collection.

In India, the size of the industrial automation industry is estimated to be US$ 2 bn while its growth rate is approximately 11.6%. This is expected to grow to almost US$ 7 bn by the 2030.

And then there are data centres.

With over 880 m internet users and a thriving technology sector, India's data centre capacity has seen a massive explosion.

It is poised to accelerate further with the rise of AI. Global cloud service providers such as Amazon Web Services, Google Cloud and Microsoft Azure have established their presence in India.

The demand for power from the data centres has grown at around 5% annually on an average. However, with demand growing exponentially there could be significant stress on the power grid.

Given the strong power demand outlook and the need to transition to green power, the government of India has outlined an ambitious capacity growth outlook for the power sector.

As per the National Electricity Plan (NEP) released by CEA in 2023, India's total installed power capacity will rise from 400 GW in 2022 to over 600 GW by FY27.

Thermal will account for 39% of this expanded installed capacity, with solar and wind making up 30% and 12%, respectively.

Further, by the end of FY32, total installed capacity is projected to rise to 900 GW, with solar and wind together accounting for 53% of total installed capacity, even as thermal's share is expected to fall to 29%.

Despite the bullish stance on the outlook for the power sector, there are some critical challenges that could hinder the performance of the companies on the stock markets.

Delays and High Debt in Adding New Capacities

The timely completion of generation and transmission projects is vital for companies to achieve their earnings targets.

However, generation and transmission companies may face issues related to land acquisition. Project delays can also be a result of supply chain issues and high debt levels for new power plants.

Low Profitability in Renewable Energy Projects

In the case of renewable energy projects, the tariff is fixed in advance for the life of the project, generally up to 25 years.

Such projects have their own set of challenges, such as lower-than-expected plant load factor (utilisation), delays in transmission connectivity, cost overruns or a quicker-than-expected decline in efficiency for solar panels/wind turbines.

Competitive Intensity

Competition has risen in power generation and transmission over the years: Given the strong capex outlook, companies across the sector have strong growth plans. Hence, competition intensity has risen over the years.

Similarly, return in equity on plain vanilla solar or wind projects, which are simpler to execute, is likely to be lower at 12-15% versus more complex projects.

Distance Between Generation and Demand Centers

As power generation sites are often far from major demand centers, substantial investments are required in transmission networks to efficiently transport electricity.

Moreover, rising costs associated with transporting coal, including the need for new rail infrastructure further emphasize the importance of cost-effective transmission.

Grid Reliability

Instances of grid failure and tripping necessitate investments in transmission infrastructure to improve resilience and prevent disruptions in power supply.

Peak electricity demand in India has grown from 164 GW in FY18 to 243 GW in FY24 clocking an average growth rate of 6.8% in the past six years.

With India being among the lowest per capital consumers of electricity, there is long runway of growth for power producers, transformers and financers and exchanges.

So, investors need to keep a watch on the old economy power stocks like NTPC for not only their own growth prospects but also upside from stakes in new age businesses.

NTPC is India's largest power utility with an installed capacity of 76,475.68 MW (including JVs).

Established in 1975, NTPC is steering ahead to be India's largest integrated power company and targets to become a 130 GW firm by 2032.

Meanwhile its IPO-bound subsidiary NTPC Green Energy aims to invest up to Rs 1 trillion in solar and wind assets by FY27.

NTPC Green Energy has an installed capacity of 3,220 MW. It is aiming to take up the same number to 6,000 MW by March 2025, and 19,000 by March 2027.

The company will operate at a level where 90% of the capacity will be solar, which requires an investment of Rs 50 m per MW, and the rest will be wind, which needs Rs 80 m per MW.

Apart from these there are several power sector stocks that can prove to be long term wealth creators if bought at the correct valuations. Check out the Equitymaster Screener.

Warm regards,

Tanushree Banerjee

Editor, StockSelect

Equitymaster Research Private Limited (formerly Equitymaster Agora Research Private Limited) (Research Analyst)

Recent Articles

- Future Engineering Stock Hidden in Golden Lustre November 27, 2024

- India's leading jewellery and branded accessories maker has a hidden ace up its sleeve.

- The Right Way to Invest in Stocks in This Market November 26, 2024

- Here's some timeless wisdom to help you navigate the stock market today.

- Beyond the Hype: The Mamaearth Lesson and the Importance of Value Investing November 25, 2024

- Why valuation and business quality matters more than hype

- A Unique Smallcap Stock for Your AI Watchlist November 22, 2024

- AI is the future, whether or not you are ready for it. To avoid missing out, here is a stock for your watchlist.

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Research Private Limited (formerly Equitymaster Agora Research Private Limited).

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Research Private Limited (formerly Equitymaster Agora Research Private Limited) (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Research Private Limited (formerly Equitymaster Agora Research Private Limited) (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Equitymaster requests your view! Post a comment on "Power Stocks: Long Term Wealth Creators". Click here!

Comments are moderated by Equitymaster, in accordance with the Terms of Use, and may not appear

on this article until they have been reviewed and deemed appropriate for posting.

In the meantime, you may want to share this article with your friends!