Hidden Potential: Can This Mid-cap Stock Double Your Money?

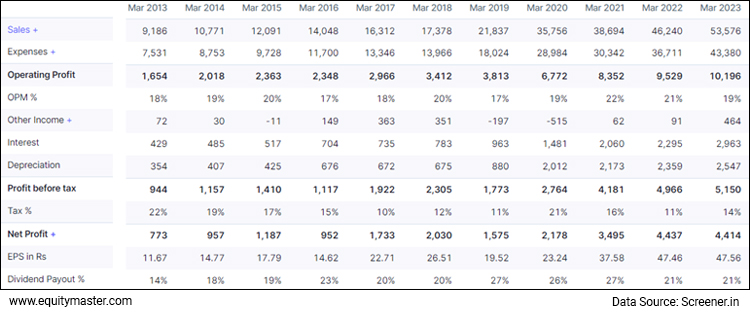

This is a P&L statement of a prominent mid-cap company.

Please focus on the performance of the company for the 10 years between FY13 and FY23.

It does look impressive, doesn't it? The topline between FY13 and FY23 has gone up by almost 6x.

The bottomline or the net profits have also gone up by a similar magnitude i.e. by 6 times.

This translates into a CAGR of 20%, which is quite good in my view.

Now, let us talk about the share price performance of this company.

You see, over the last 10 years, the stock market has given this company a PE multiple of 18x on average. Please note I'm talking about the average PE multiple.

There have been occasions where the PE multiple has gone to as high as 35x and there have been occasions where it had gone to as low as 12x.

On average though, the multiple has stood at around 18x.

If you would have noticed, the earnings per share or the EPS of the company in FY23 was around Rs 50 per share. It was the same in FY22 also.

--- Advertisement ---

Investment in securities market are subject to market risks. Read all the related documents carefully before investing

Top 2 Stocks to Ride India's Bluechip Bull Run

Our co-head of research, Tanushree Banerjee's research hints at a potential mega bull run in bluechip stocks over next several years.

She has already identified her top 2 stocks to ride this emerging opportunity.

You can discover everything about this mega opportunity in this detailed note from Tanushree.

See Full Details Here

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.com

---------------------------------------------------

The math is therefore simple. Earnings per share of Rs 50 multiplied by a PE multiple of 18x gives you a fair value of around Rs 900 per share.

This means that based on historical average PE multiple and the company's earnings power, a rational investor would buy the company at Rs 900 per share or lower.

Assuming that the company is able to grow its earnings by 15% as opposed to the 20% historically and the buying price of the investor of Rs 900 per share, he can hold the stock for 3-5 years, earn his returns of 15-20% per annum and then exit if he wants to.

He can sell the stock at the same multiple of 18x if the fundamentals of the company remain intact.

Here's the surprise though. This stock is currently trading in the market at just Rs 480 per share.

Yes, that's correct. Mr Market is not valuing the stock at Rs 900 per share but is valuing it at a much lower price of Rs 480 per share.

Now, there are a couple of reasons on why Mr Market is devaluing the stock so much.

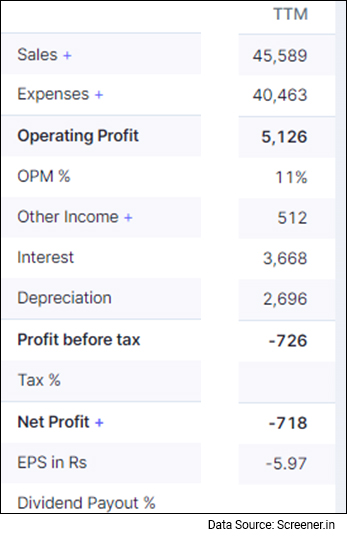

The first reason is the performance of the company in the last 12 months. The performance is disappointing to say the least.

As you can see, the company has incurred a loss of Rs 718 crores in the 12 months ending December 2023.

This loss has occurred because of one of the worst slowdowns the industry is facing in decades.

The company is hurt not only on the topline front where both volumes as well as realisation are down, the profitability has also taken a hit due to increase in rebates and sizeable revaluation of inventory.

Value Stocks: For People Who Never Like Overpaying for Anything

Hence, from a consistent 18-20%, the operating margin has fallen to 11% during trailing twelve months.

And this is one of the main reasons why the stock is trading at just Rs 480 per share as the losses have spooked investors.

There's another reason why investors seem to be worried. And it is to be found on the balance sheet of the company.

There are two things that stand out when you look at the balance sheet of this company. First, the debt-to-equity ratio has been well under control till FY18.

It has remained below 1x between FY12 and FY18.

The second thing is that the debt-to-equity ratio has shot up suddenly in FY19 from Rs 6,600 crores to a whopping Rs 29,139 crores. That's a jump of almost 4.5x.

What explains this huge jump in the debt levels of the company?

Well, a company did a leveraged acquisition in FY19 worth around Rs 30,000 crores.

Yes, that's correct. It paid close to Rs 30,000 crores to buy a company called as Arysta Lifescience to deepen its global footprint.

And around 70% of this acquisition was done through debt. In other words, the company had to take on debt of more than Rs 20,000 crores in order to generate funds for the acquisition.

And it is this debt that has remained on the company's balance sheet since then. In fact, the total debt has gone up marginally from Rs 29,000 crores in FY19 to around Rs 35,000 crores currently.

To be fair to the company, while the overall debt levels have gone up, the debt-to-equity ratio has come down from 2x in FY19 to 1.4x in September 2023. So, the effort towards deleveraging is certainly being seen. It must speed up more in my view.

As we just saw, a rational investor would pay Rs 900 for this stock but because of the huge losses in the last 12 months and the high leverage, the company is currently trading at Rs 500 per share.

The million-dollar question therefore is whether the company would return to its old profitability and growth.

--- Advertisement ---

Investment in securities market are subject to market risks. Read all the related documents carefully before investing

Choose Your Pick

Unnecessarily Risky Small Caps vs Small Caps Brimming with Opportunity

Discover the Small Cap Strategy Thousands of Equitymaster Subscribers Use

I'm interested

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.com

---------------------------------------------

And if yes, how soon? Also, will leverage be further bought under control?

I have read a little bit on the company and here's what I found.

The management expects to return to mid-single digit growth in revenues and profits in FY25 and from FY26 onwards, it expects to get back to its old growth of 15-20%. So yes, the company will start growing again by F26 if you believe the management.

Besides, the company's debt levels are also expected to come down on account of initiatives like receivables factoring and stretching of creditors.

It is also proposing to raise equity worth Rs 4,000 crores by way of rights issue in order to reduce debt.

These are all positive signs indeed. Not only is the profitability and growth expected to return by FY26, the debt levels are also expected to go down.

In other words, if things go as per the planning of the management and if Mr Market again values the company at the same PE multiple as it has done in the past, there is a strong chance for the stock price to touch Rs 900 or so levels again.

Of course, this is not advice or recommendation to buy the stock. I'm just highlighting one of the many scenarios possible and you are advised to do your own research.

I'm sure you are wondering why have I not revealed the name of the stock yet?

Well, if you haven't guessed by now, the stock is none other than UPL Ltd, among the top 5 agrochemical companies in the world.

Some of you may find my analysis shallow and not up to the mark.

You may wonder where is the analysis of the company's different products and their market share, where is the industry analysis and also, why there is no mention about the management and the future prospects of UPL?

Well, I would like to point out that whatever qualitative information I needed on the company, I have found most of it in the historical financials of the company.

You can make out from the historical financials that the company seems to be doing a good job of growing both volumes as well as realisations.

You can't grow at 20% per annum by growing volumes or realisations alone. Both need to contribute.

I am also impressed by the consistency in operating profit margins which tells me about good control on costs as well as decent pricing power.

Yes, it did make a dubious decision by going in for a leveraged buyout which led to its debt levels exploding. However, it seems to be working hard to bring debt under control.

As to the future prospects, I am not expecting something extraordinary from the company.

All I am expecting is for it to return to its old growth trajectory of 15-20%, which it is capable of achieving as it has managed to do the same in the past.

Yes, if I was expecting the company to grow at 25-30% then it is a different story. But I believe it has the systems and processes in place to grow at its historical rate of 15-20%.

I believe this much qualitative understanding is enough if the company has a long history and if the valuations are reasonable.

This much understanding is enough to minimise losses if things don't go as per plan or a turnaround is taking longer than usual.

Lastly, you also have portfolio diversification where you have a portfolio of 20-30 stocks so that even if a few stocks don't work out, you would still be fine because your portfolio is spread across a large number of stocks.

Thus, in conclusion, the risk-reward equation in UPL appears quite decent from a rational investment perspective provided the company returns to its old growth and profitability and the stock market rewards it with its old PE multiple of 18x.

Remains to be seen if it retests those high levels again or there is more pain in the offing for shareholders.

Happy Investing.

Warm regards,

Rahul Shah

Editor and Research Analyst, Profit Hunter

Equitymaster Agora Research Private Limited (Research Analyst)

Recent Articles

- A Simple Hack to Beat the Big Investors for Multibagger Gains May 3, 2024

- Forget the earnings season. Here's is a better metric that could offer interesting insights about stocks.

- How to Invest in Indian Semiconductor Stocks May 2, 2024

- Is this the right time to invest in semiconductor stocks?

- After Tata can This Business Group Create Wealth? May 1, 2024

- Aditya Birla Group announces multiple strategic decisions. How can you profit?

- Best Transformer Stocks for Your Watchlist April 30, 2024

- How to profit from the transformer gold rush.

Equitymaster requests your view! Post a comment on "Hidden Potential: Can This Mid-cap Stock Double Your Money?". Click here!

1 Responses to "Hidden Potential: Can This Mid-cap Stock Double Your Money?"

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Raju VSK

Apr 28, 2024Excellent review